Cobre Panama Project Risks High for First Quantum Minerals

Summary

First Quantum Minerals is a C$21B Canadian copper miner with assets in Africa, Europe, Australia and Latin America.

The company has strategic ambitions to produce 1Mt of copper in the near future.

Yet wide ranging issues, particularly linked to a public spat with the Panamanian government may lead to a sizable reduction in volumes.

Company Overview

First Quantum is a Canada based copper focused miner with South African heritage and a focus on expanding its nickel portfolio. Its operations spanning parts of Africa, Europe, Asia, Australia, and Latin America has pushed copper production beyond 700kt per annum.

With copper representing 88% of sales, the firm is set on expanding nickel output with select investments in certain projects. The copper miner’s strategic ambitions sit squarely focused on producing 1m ton of battery grade minerals over the next 5 years. To do so, the firm is considering the development of underground copper plays such as Las Cruces project in Spain.

The company distinguishes itself through its in-house construction and project design capabilities, fast-tracking project go-live and providing project flexibility. The First Quantum model covers all front-end project design and execution phases, engineering, procurement, and construction management.

However, all is not rosy at the C$21B copper miner. A public spat with the Panamanian government over Cobre Panama, a possible revision in Zambian royalties and even inclement weather has conspired to impact production output.

At 26x forward earnings, and with risks related to copper production due to a possible shutdown of the Cobre Panama project, it is presently hard to endorse the company. While not an outright short sale target, my outlook remains relatively bearish. Accordingly, I maintain a hold rating on the equity.

Copper prices have recently moved to the upside following a mid-year lull driven by fears of a slowing global economy.

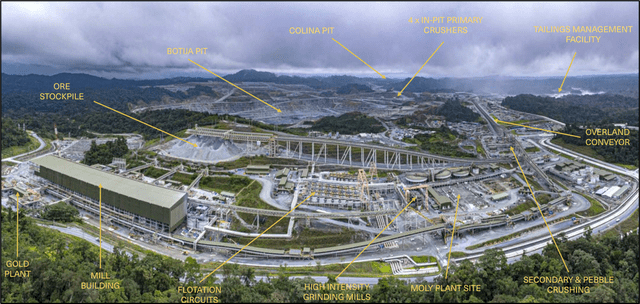

Cobre Panama

First Quantum’s involvement in the prolific Cobre Panama copper play pre-dates 2013. At that time, project concept had little chance of succeeding for a multitude of issues including copper grade, geographic conditions, and labor skills. At that stage, the firm undertook the project on the proviso the Panamanian government would support the project with attractive fiscal incentives.

The project has comparably lower ore grades than other copper mines in Chile or Peru, inflating project costs and pressuring economic viability. Harsh terrain and meteorological conditions meant that project construction phases were hampered, and skilled labor shortages incurred project delays.

US $10B in capital expenditure has been ploughed into the project to develop it yet a steep rise in government levies is now threatening project shutdown. The company holds firm that no other option but to close the vast copper project avails if it does not resolve a sizable tax dispute with the Panamanian authorities.

Any Cobre Panama expansion is likely to be mothballed, perhaps cutting group production by 50% if an agreement cannot be found on taxes and royalties.

On one side, the Panamanian government has demanded the copper miner pays $375M per year along with a profit based mineral royalty of 12%-16%. This is sizably more than previously paid by First Quantum Minerals which disbursed $61M in 2021, despite the project raking in $1.4B in gross profit.

The Panama government claims it was obliged to renegotiate the project’s original 1997 contract following a ruling by the country’s supreme court declaring it unconstitutional.

Significant capital has already been committed to development of the project.

The stakes are exceedingly high, not only for the Panamanian copper project, but for the battery mineral itself with Cobre Panama copper production responsible for 1.4% of global supply.

The project contributes 5% of national GDP, 75% of Panama’s exports and provides economic support to circa 100,000 Panamanians. Any enduring disruption is likely to pressure copper prices to the upside.

Company Financials

Amid a tighter credit environment, debt reduction remains a priority for the Canadian mining company. Last twelve months debt to EBITDA rating hit 2.3x, a meaningful reduction from FY 2019 (6.2x) and FY 2020 (4.5x).

Understandably, leverage remains a concern, particularly given interest rate rises impacting the firm’s profitability. First Quantum Minerals retains a 0.51% dividend yield, albeit a minimum annual base dividend of C $0.10 per share and a performance dividend based on 15% of available cash flows.

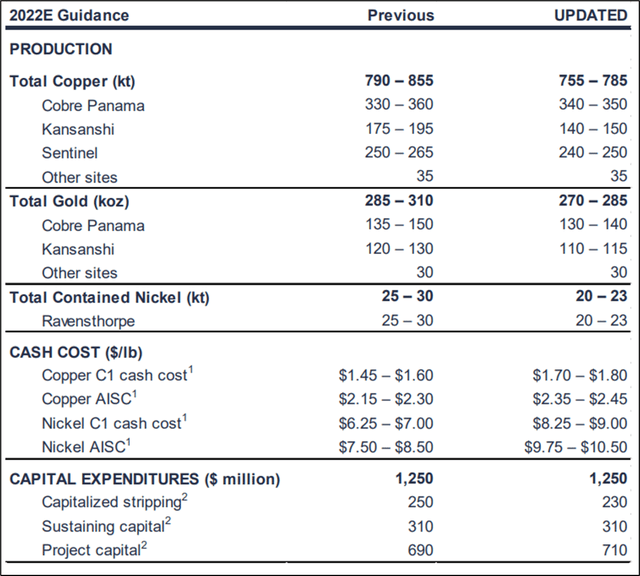

Copper guidance was lowered at the back end of 2022, attributable to lower production at Kansanshi. Since then, notable disruption has occurred at Cobre Panama following disagreement on royalties with the Panama government. Notably wet weather has also impacted volumes, most recently in Zambia.

Production guidance has been lowered and a range of costs revised upwards related to inflation, increased labor costs, and capital expenditure.

Q3, 2022 revenues totaled $1.7B, down 9% on a quarter over quarter basis. Margin compression was felt across the business as weak metal prices combined with higher input prices to drag on margins.

Group EBITDA margin dropped to 34% from a high of 54% in Q1 earlier in the year. The $583M in reported EBITDA was down 36% quarter over quarter with a paltry $113M in net earnings, compared to $419M in net earnings only a quarter earlier.

Gross profits halved, from $629M (Q2, 2022) to $302M (Q3, 2022) With a range of operational issues and inflationary pressures hitting cash costs, future print does not look much better.

The firm presently holds US $1.789B in cash and marketable securities, marginally lower on a quarter over quarter basis. Receivables have slightly moderated to the upside, from US $368M (2Q, 2022) to US $445M (3Q, 2022) with inventory flatlining around US $1.45B.

First Quantum Minerals is holding US $237M in goodwill on its balance sheet linked to past acquisitions. While this is not presently meaningful on assets worth US $24B, it is worth keeping an eye out for annual testing for impairment that may ultimately hit equity.

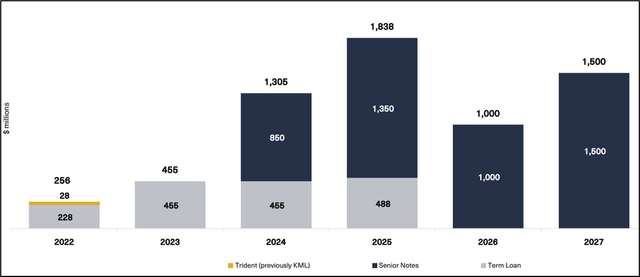

Debt maturities are set to escalate into the second half of the decade.

Little has changed in long term debt over the year, printing at US $7.79B while management looks to make inroads into overall reduction. US $367M of long-term debt was repaid in Q3 and rolled over, with another US $309M being issued. So far this year, US $75M in dividends have been distributed.

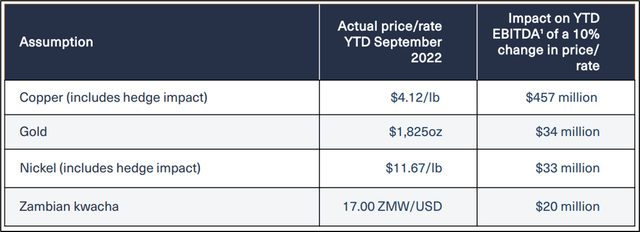

First Quantum Minerals is naturally exposed to changes in copper prices with a 10% increase/ decrease equating to $457M impact to EBITDA.

First Quantum minerals trades at 26.2X earnings over the next twelve months, that’s slightly higher than the much bigger Freeport-McMoRan (FCX) (23.4x) particularly given the US $64B American copper giant posts comparably better returns on assets (9.97% v 5.99%), returns on total capital (14.40% v 7.20%) and returns on common equity (27.34% v 11.34%).

While EBITDA margins remain roughly the same at ~45%, the giant American miner converts cash more quickly (53 days v 72.4 days) and has significantly less debt/EBITDA (1.1x v 2.3x).

In summary, there is not a lot to justify why First Quantum Minerals trades at a relative premium, particularly given the multitude of different issues facing the company.

Risk Factors

An extensive set of unknowns face the Canadian copper miner, none of which is probably bigger than the public spat between the Panamanian government and the company over Cobre Panama royalties. A worse-case scenario fall out could see the company suspend operations, cutting overall copper production by almost 50%.

Expropriation of the asset, while unlikely, could lead to costly write-downs and a re-thinking of group strategy. Given these factors, it is hard to see how the company is trading at a premium to the much bigger Freeport-McMoRan, for example.

The company is running higher debt levels, so credit risk does play a factor, specifically at a time where a strategic de-levering takes place when cash available to do so dries up.

Key Takeaways

First Quantum Minerals presents an interesting opportunity for money managers to allocate capital to a copper industry in take-off mode. However, multiple risks present themselves.

While a softening of the $US dollar is likely to support prices in 2023, the outlook remains somewhat cloudy. Cobre Panama’s future remains in a state of flux, a renegotiation on royalties with the Zambian government is perhaps on the cards and inclement weather has recently been impacting Zambian mining production. All this makes for perchance an expensive buy at 26x forward earnings.

![]()