Kagem releases updated ‘G-Factor for Natural Resources’ figures to 31 December 2025

Kagem Updates G-Factor for Natural Resources Figures for 2025 Year-End

Gemfields, which operates Kagem Mining Limited (“Kagem”) in Lufwanyama, is pleased to confirm its ‘G-Factor for Natural Resources’ figures for Kagem, which now stand at 17% for the 10-year period from 2016 through 2025.

The ‘G-Factor for Natural Resources’ reveals the percentage of natural resource revenue paid to the government of the host country in the form of mineral royalties, corporation tax and, where the relevant government is a shareholder, dividends.

First announced in 2021, Gemfields shares its ‘G-Factor for Natural Resources’ annually in an effort to promote greater transparency and accountability regarding the level of natural resource wealth shared with the host country’s government, whether that value originates from the mining, oil, gas, timber or fishing sectors. It is also an indicator of the efficiency of natural resources companies in converting those natural resources into funds for the host government.

Gemfields’ CEO, Sean Gilbertson, said:

“Gemfields’ 2025 G‑Factor for Natural Resources for Kagem underscores how contributions to host nations vary with market and operating conditions.

“At Kagem in Zambia, the one‑year G‑Factor for Natural Resources was just 6% for 2025, far below its long‑term average.

This reflects the halt in mining operations at Kagem from January through April 2025 as a result of competitor actions in the market and the temporary 15% export tax on precious gemstones, which was lifted by March 2025.

With operations restarted and market conditions improving, we expect Kagem’s G‑Factor to trend back toward its long‑term average of around 18%.

“We remain committed to the transparency provided by the G‑Factor for Natural Resources and continue to encourage broader industry adoption so that host governments and their citizens can better assess the stewardship of their resources.”

The ‘G-Factor for Natural Resources’

The G-Factor for Natural Resources would typically be calculated by each standalone company engaged primarily in the extraction and sale of natural resources, whether in the mining, oil, gas, timber or fishing sectors.

Accordingly, multi-national natural resource companies would publish the G-Factor for Natural Resources for each operating subsidiary engaged primarily in the extraction and sale of natural resources.

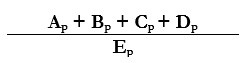

The G-Factor for Natural Resources is expressed as a percentage and is calculated as:

where:

- A = the total mineral royalty (tax on revenue) paid by the reporting company to the host country government during the period

- B = the total corporation tax (tax on profit) paid by the reporting company to the host country government during the period

- C = the dividends paid by the reporting company to the host country government during the period (where the host country government is a shareholder in the reporting company)

- D = the total export taxes or export levies paid by the reporting company to the host country government during the period

- E = the total revenues of the reporting company during the period

- p = the relevant period, typically calculated for each of (i) the prior year; (ii) the preceding 5 years and (iii) the preceding 10 years

- The sums actually paid during the period (rather than the sums accrued or falling due during the period) are used for the purposes of A, B, C and D.

No measure of this type is perfect and it is recognised that:

- the G-Factor for Natural Resources is a “rule-of-thumb” – while it has broad application and is a practical indicator, it is not suited to every situation;

- there are numerous additional and indirect taxes which are not included in the G-Factor for Natural Resources and which further increase the contribution made to host nations by natural resource companies. Such taxes include but are not limited to area/surface charges, social security contributions, taxation on the salaries of employees, import and export duties, VAT, etc; and

- the variety and variations in natural resource deposits, types and occurrences lessens the ability to make direct comparisons between companies.

![]()